Why Risk-Adjusted Returns Matter and How Low Vol Equities Might Help

Most investors either explicitly or implicitly understand the importance of risk-adjusted returns. This is shown by the fact that investors typically diversify to shield their portfolios from uncompensated risk. If risk was not an important consideration in portfolio construction, allocating all assets to a single security with the highest expected return would be quite common. Instead, nearly all investors are risk-aware and choose to hold other assets with lower expected returns in order to reduce the overall risk of their portfolio.

The evidence is clear when looking through an asset allocation lens: in addition to equities, nearly all institutional investors hold bonds, which typically carry a lower expected return but also incur lower volatility than equities. A mixed allocation to bonds and equities signals a general risk awareness and a degree of risk aversion. It's important for investors to get compensated for the risk they incur, and the Sharpe Ratio - a measure of risk-adjusted returns - serves as a barometer for that.

Risk/Return Profile of Low Vol Equities

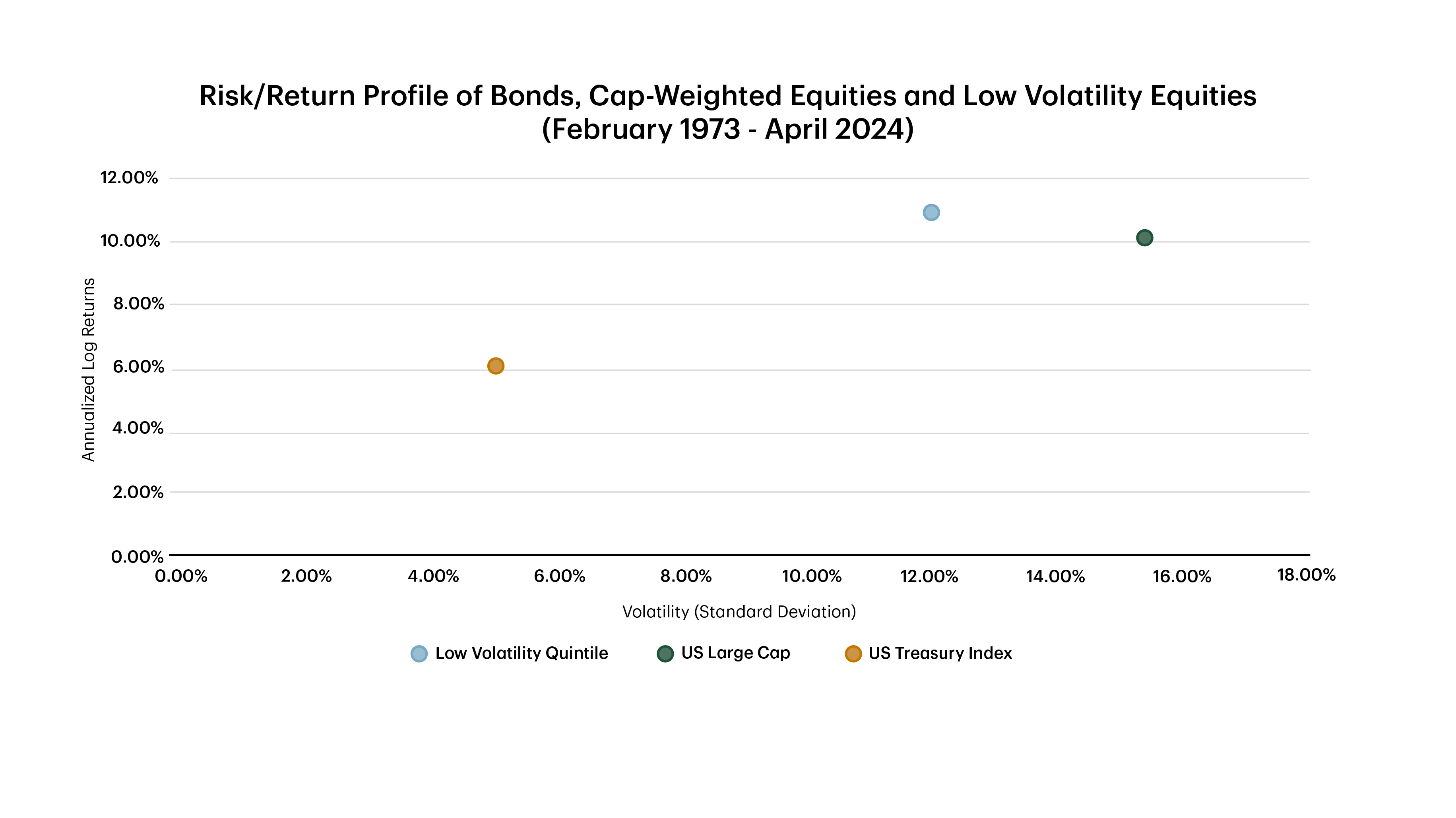

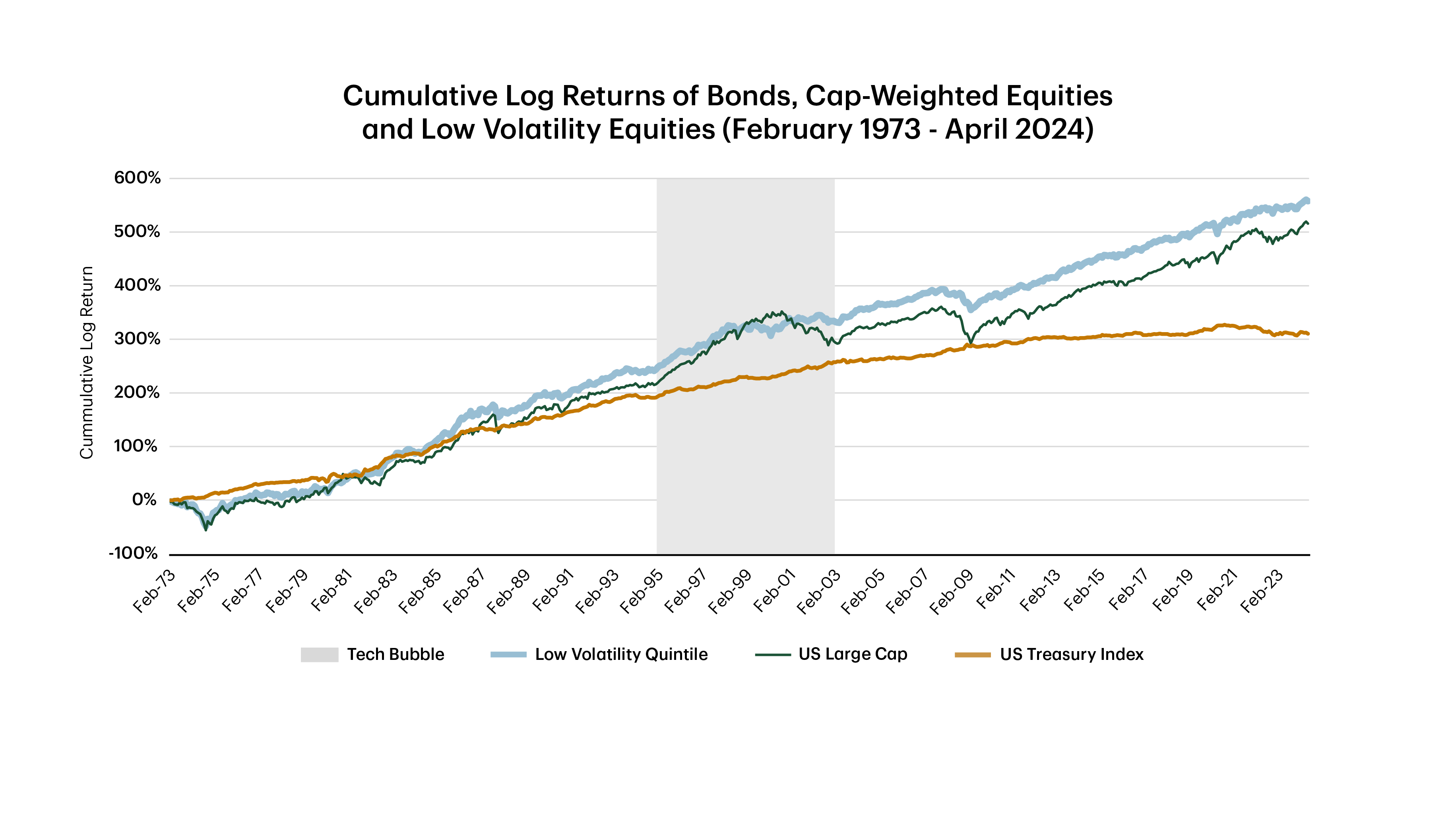

Low volatility equities are no different than any other asset class and should be treated as such when considering strategic asset allocation. Based on long-term empirical evidence in every market around the world, low volatility equities deliver, over the long run, returns that are comparable with broad-based stock indices weighted by market capitalization (capitalization-weighted indices), with meaningfully less risk. Therefore, they have the potential to offer a more attractive way to gain exposure to equities from a risk-adjusted perspective.

Some investors have difficulty grasping this concept because they don't look at low volatility equities in terms of their absolute risk, but rather in terms of their active risk against the market, which can lead to making erroneous strategic asset allocation decisions. This irrational human behaviour is a reason why the low volatility anomaly persists to this day.

Source: Kenneth R. French Data Library, Bloomberg Finance L.P., TDAM. As of May 31, 2024.

Source: Kenneth R. French Data Library, Bloomberg Finance L.P., TDAM. As of May 31, 2024.

In addition, the potential ability of low volatility equities to protect on the downside may provide better capital preservation than cap-weighted indices on average during down markets. This is particularly helpful for institutional investors because it may allow them to better meet their future obligations in challenging market environments. Low volatility equities may help investors consistently pay the bills.

Source: Kenneth R. French Data Library, Bloomberg Finance L.P., TDAM. As of May 31, 2024.

Source: Kenneth R. French Data Library, Bloomberg Finance L.P., TDAM. As of May 31, 2024.

Navigating the Uncertain Market Outlook

Low volatility investing has faced significant headwinds recently in comparison to cap-weighted indices, primarily due to a small number of companies driving cap-weighted returns and leading to highly concentrated outcomes both from a risk and return perspective. It would be great to predict the near-term performance of low volatility equities and the market, but an accurate forecast would require nothing short of clairvoyance. While low volatility equities offer some reasonable visibility into their future return due to the low dispersion of their outcomes, the market is much more volatile and offers much less visibility. With market risk concentration at an all-time high, the outlook for the market hasn't been this uncertain in the last two decades.

Low volatility equities are not benchmark-centric. They offer a distinct way to invest in equities, with much lower risk than the market. However, this comes at the cost of much higher benchmark-relative risk compared to cap-weighted indices. The very premise of low volatility is that risk reduction can be achieved without sacrificing long-term returns, but this also means that predicting whether low volatility will outperform the market over the short term becomes a much more difficult question to answer.

This is why instead of focusing on the short-term probability of outperforming an already frothy market, investors would be better served if they adopt a longer-term focus, get exposure to the equity market with less risk and obtain better risk-adjusted returns.

For institutional investment professionals only. Not for further distribution.

The information contained herein is for information purposes only. The information has been drawn from sources believed to be reliable. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance.

This material is not an offer to any person in any jurisdiction where unlawful or unauthorized. These materials have not been reviewed by and are not registered with any securities or other regulatory authority in jurisdictions where we operate.

Any general discussion or opinions contained within these materials regarding securities or market conditions represent our view or the view of the source cited. Unless otherwise indicated, such view is as of the date noted and is subject to change. Information about the portfolio holdings, asset allocation or diversification is historical and is subject to change.

This document may contain forward-looking statements (“FLS”). FLS reflect current expectations and projections about future events and/ or outcomes based on data currently available. Such expectations and projections may be incorrect in the future as events which were not anticipated or considered in their formulation may occur and lead to results that differ materially from those expressed or implied. FLS are not guarantees of future performance and reliance on FLS should be avoided.

Bloomberg and Bloomberg.com are trademarks and service marks of Bloomberg Finance L.P., a Delaware limited partnership, or its subsidiaries. All rights reserved.

TD Global Investment Solutions represents TD Asset Management Inc. (“TDAM”) and Epoch Investment Partners, Inc. (“TD Epoch”). TDAM and TD Epoch are affiliates and wholly-owned subsidiaries of The Toronto-Dominion Bank.

®The TD logo and TD other trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.

Related content

More by this Author